The GameStop (GME) debacle garnered a lot of attention. Some people consider the problem to be centralized systems. According to these critics, the shortcomings of today’s financial system could possibly be solved by decentralized Blockchain alternatives.

Robinhood’s trading app came under fire after trading restrictions were imposed on its users. As more brokers followed suit, it sparked an outcry in social media groups, and among elected government officials. Concerned parties suspected an attempt by Wall Street to protect itself against newly empowered populist investors.

Depending on one’s perspective, the debacle revealed, on the one hand, the power that large institutions can wield over retail investors when the market acts against their bets. On the other, it revealed connections that displayed astonishing conflicts of interest in the thoroughly regulated industry. However, it also revealed how an organized movement as a mass can influence and profit from the financial market.

The approaches of Blockchain technology and the implementation of those in the world of decentralized financial applications (DeFi) could offer direct solutions here. The technical state of decentralized exchanges is currently far from being able to handle order matching capacities of traditional trading venues. However, new implementations and scalability improvements are likely to bring huge quantitative improvements in the future.

Where traditional finance can pick up valuable inspiration from their decentralized market peers, however, is in governance structure, changeability, incentivization, democratization of supply, and availability, for example. With a Decentralized Exchange (DEX), users have a high level of responsibility, which is rewarded with digital self-determination.

The Comfort Trap

After a simple promise and with possible prospects of profits, many are tempted to grab the opportunity by the hand. Few consult the terms and conditions or even care about the privacy policy of the smartphone app to be installed. The promise to simply participate in stock trading with small money, and perhaps also to profit once from the profits on the stock exchange, is all too tempting.

Free is often not free, and free is not always free, as Google and Facebook, for example, have shown us in recent years. Freemium offers entice with free offers, but often take away the right to do business with the generated data. Often, this right is not removed with a paid offer and the provider earns twice from each user.

Democratization Of Finances For All

A financial app called Robinhood, known as a champion for social justice, virtually implies taking from the rich to give to the poor. But it should not be forgotten that they relay real-time information to so-called “market makers” in the background about the stocks users are buying and selling. It’s a practice that some regulators and industry observers have previously viewed as a potential conflict of interest.

Robinhood and other brokers cannot execute buy/sell orders directly, and are therefore required by law to work with market makers who can offer their brokers the best market prices for a given trade. When Robinhood forwards a transaction to one of these third parties, the market maker learns which security is being bought or sold – before the actual trade takes place.

Citadel: Significant Market Maker

When a large buyer establishes a position and starts buying, prices tend to rise because there is limited liquidity. Also, sellers are often smart and know they can raise prices if someone needs a lot of shares. In short, it’s profitable to join the party when you know others are buying.

Citadel and other market makers pay Robinhood a small fee for the privilege, which gives them real-time information about retail trading patterns. Citadel says they use this information to improve their trading algorithms.

High Frequency Trading – Frontrunning in the Milisecond Range

Robinhood is a fintech company where stocks can be traded for free. The cost structure gives them the advantage over competitors who have to charge a fee per trade. They get most of their revenue by routing orders to high frequency trading firms (HFTs). These firms specializing in HFT “see” the customer orders placed and buy or sell the same number of the order already in the market to settle it a few units higher to the customer.

All this happens with the use of powerful computer programs in the range of milliseconds, and cannot be seen by the naked eye. Thus, the high frequency trading profits every time customers of brokers forward their order flows to HFT and send an order to the exchange. This transaction is more or less risk-free, since the position entered can be settled mili-seconds later to the original orderer. If this would happen manually and one would profit from the information of a buy or sell order, it is illegal and will be punished as so-called frontrunning.

The revenue Robinhood Securities receives from the third-party marketplaces is shared according to a fully disclosed clearing agreement with Robinhood Financial LLC. The per share amounts represent the total amount of payments received from Robinhood Securities (Options Order Routing). Payments vary based on a fixed percentage of the spread of the respective trading venue.

Bitcoin – a new system?

Bitcoin paved the way for an alternative financial system with its algorithmic monetary policy. Unlike traditional finance, Bitcoin as a network is resistant to censorship and its money creation cannot be manipulated. It creates a real, unbiased yield curve for the Bitcoin (BTC) asset, which is used as collateral in numerous financial applications in the DeFi space.

With a wallet, crypto assets are independently and self-determinedly traded, held or safely stored. Via smart contracts, the assets held can not only be traded directly on decentralized exchanges, but ownership can also be mortgaged. This is likely to be close to the interest rates of the old banking system. Liquidity is needed in the decentralized financial system, which is provided by innovative instruments (DeFi). Lenders are remunerated by the smart contract, but also secured.

The trust lies in the open source code of the provider, which (usually) publishes its program code. This is checked by experts (audit) and can be assessed by all possible users. Security experts and hackers are invited via bug bounties to crack the code before it is publicly implemented. Thus, most bugs are detected before the smart contract is actively deployed. Still, there is always some risk; code is almost never bug-free.

The Era Of Decentralization

Decentralization can usher in a new era, democratizing the trading of value in addition to finance. In decentralized, censorship-resistant trade, the market (supply/demand) will rule. Of course, information and “fake news” can still move markets unnaturally. However, centralized registries are more vulnerable to cyberattacks, fraud, and censorship because there is a single point of failure and nodes are operated by selected parties.

The transparent (DLT) registry of a Blockchain is distributed across thousands of nodes, which can be operated and connected by anyone on inexpensive hardware. In times of dwindling trust, some are willing to take responsibility into their own hands and participate in the new system. The rising prices of infrastructure tokens, exchange currencies and the exodus of Bitcoin assets on exchanges may reflect this trend.

DeFi Requires Open Banking

Innovative financial instruments in the field of decentralized finance (DeFi) are still in their infancy, and yet risky experiments have already yielded telling results. This has aroused the interest of a large crowd that feels disadvantaged by the current financial system and is looking for an alternative.

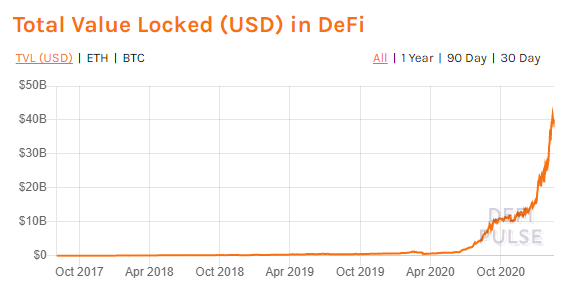

A quick look at the data explains why this trend has appeal. The total value deposited in DeFi protocols is at all-time highs, currently reaching over $40 billion. Moreover, efficient finance on the Blockchain is open banking per se. When everyone can freely participate in the market, there is no middleman required.

*Originally posted at CVJ.CH